It's still Tiger's World; $12billion for Andy Gardiner's thoughts; No Questions Asked, football and crypto; PIF will be LIVid; All Blacks in red; eKloppnomics; The Jay Monahan Trust Exercise

Overthinking the sports business, for money

Stuck. Decoding golf’s new, new future

What happened?

Eight months after the proposed framework agreement between the PGA Tour and the Saudi Public Investment Fund was announced, the Tour has finalized a $3 billion deal with Strategic Sports Group (SSG) to create PGA Tour Enterprises, which houses the commercial rights of the US and European Tours.

It remains to be seen whether PIF comes on board down the line.

See below, the story in pictures.

Then:

Now:

PIF’s absence keeps the LIV disruption story in play.

So we remain stuck.

A boring status quo and a crap breakaway.

Not quite the Kodak case study oft-referenced by the disruptor fanboys.

Poached Rahm anyone?

LIV’s Jon Rahm transfer last month can now be seen as a PIF power move in response to the news in November that Monahan was talking to SSG.

Rahm’s a good player but is he really a needle mover, particularly in the US?

We’ll see I guess, as the Spanish player sets about launching his own LIV team franchise (why are these so crap btw?).

Two Man Uniteds

There’s an interesting bit in here about valuation and revenue share models.

The tour values the new entity - PGA Tour Enterprises - at $12billion…or roughly two Man Uniteds in today’s money.

Does this ring any bells?

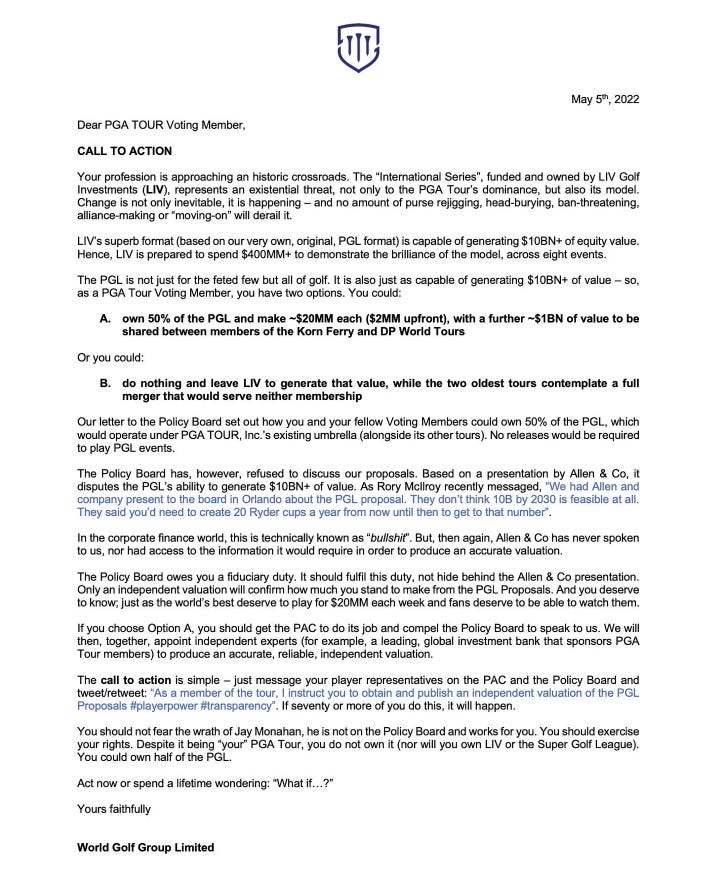

Go back 18 months and the players were weighing up a similar offer from Professional Golf League, the LIV rival.

PGL’s letter to the Tour players was a belter, quoting Rory McIlroy, who at that point was the PGA Tour’s human shield:

‘We had Allen & Co present to the board in Orlando about the PGL proposal. They don’t think 10billion by 2030 is feasible at all. They said you’d need to create 20 Ryder Cups a year from now until then to get to that number’.

So 12billion is the number today, but 10billion was ridiculous 18 months ago.

Step forward Commissioner Woods

The detail reveals where the power really lies.

The new deal has an equity share for the players, aka the bribe to keep the talent from ‘doing a Rahm’ and jumping over to LIV.

There are three numbers worth noting.

The tour has 200 member players (how many sell tickets? 5?).

There’s a $1.5billion player equity pot.

Tiger Woods is currently 887 in the Official World Golf Rankings.

So how to cut the cake?

The shares will be based on the following criteria, (AND IN THIS ORDER)….‘career accomplishments, recent achievements, future participation and services’

Given Tigers’ agent Mark Steinberg helped negotiate the deal, we can surmise that his client’s past performance is weighted very heavily indeed.

27 years after his first Masters win and with one good leg, Tiger remains by far the most valuable name in golf.

And that might be a problem that no amount of money can solve.

See also: Frankenstein, McKinsey and Greg Norman: LIV Golf is sport by numbers

Hear our conversation with Andy Gardiner, creator of PGL.

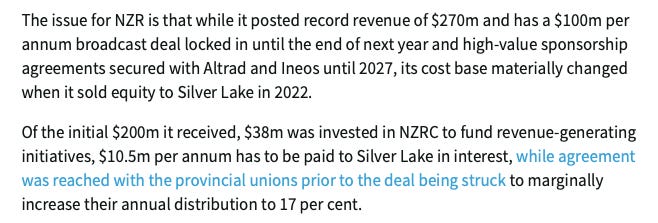

All Blacks, Red Ink

Spoiler: The Silver Lake money wasn’t free

Hear Will Greenwood questioning the role of private equity in rugby, in our recent podcast.

Q. What do Chelsea and Jordan Henderson have in common?

A. Trading reputation for money and then not getting paid anyway.

From this week’s podcast with Martin Calladine, author of No Questions Asked: Football’s Role in the Crypto Con.

“Chelsea signed a 30 million pound deal with Whale Fin, which was a crypto exchange and canceled that six months later, supposedly not having had a penny. Inter Milan had a 40 million Euro a year shirt sponsorship with DigitalBits, which they went 18 months without getting a penny from.

Putting a price on Klopp

More specifically, how much of the asset value of Liverpool is attributable to Jurgen Klopp successful reign as manager?

As someone who’s written a book questioning the role of leadership, it’s a question I tussle with.

Liverpool has been sold twice in the last twenty years. So we have two real valuation moments.

2007 - £219million (Moores family to Tom Hicks and George Gillett)

2010 - £300million (Hicks/Gillette to Fenway Sports Group)

The 2024 price point is for smarter brains than mine.

But, £2 to 4billion??

So a 10x increase in 15 years.

Going back to the initial question, how much of that increase is due to on field success and the associated brand value that comes with it?

Or is onfield performance a marginal contributor to value (cherry/cake), the bulk of which is about media rights outlooks and theories around monetising fan bases at home and abroad?

In other words, what would the price of Liverpool be if Roy Hodgson/Brendan Rogers/whoever was still in charge, and the club had spent the last few years in mid to high table obscurity - no Champions League win, no Premier League title.

UP Coming

Some podcasts heading your way soon:

If Netflix Ran Sport

When UP met Roger Mitchell

The best football club owner you’ve never heard of

That Taylor Swift Super Bowl

The Cookiepocalypse

Till next time.

Press the Like button, it’s compulsory.

The corporate smoke & mirrors at the PGA Tour would make Mandrake blush. What did SSG buy? What assets/rights has PGA Tour sold them? The deal either makes PIF/LIV very angry (unwise to poke sticks at predators) or there is a sweetener to be revealed. Like it's Middle East geopolitical "strategy" the US can't decide if Saudi is a deadly enemy or essential ally. (Houthis & Oil - yes; China, Israel, 9/11 & human rights - no.)

And what of the role of the presumptive President in all this? His son-in-law's hedge fund is flush with Saudi money and Donald owes LIV favours while the PGA Tour trashed his brand. Not a man who easily forgets.

SSG, PIF and Trump will all get their pound of flesh out of US pro golf - but whose arms and legs are disposable? The NZ rugby example is small scale proof of concept. Ultimately it comes down to current charitable beneficiaries & PGAT employees (low hanging fruit); then subsidiary tours (KFT, DP, Champs); then protected status of players outside top 50 (steeper pyramid with hungrier dogs); and finally consumers in gamblification; streaming costs; and tax/investment rorts/restructuring.

It's golf Jim, but not as we know it.