Sportel Diary; Which one are you again? Fun with OTT differentiation; The ESPN v IMG after party face off; Is ESPN worth $25billion; SportelMan; YouTube's $14bn NFL bet; Croker's Partridge moment

Overthinking the sports business, for money

(Pro tip: Press Load All Images above to get the UP Newsletter in full visual effect).

The Unofficial Sportel Diary

This week UP has been in Monaco for the sports media and tech convention.

We started with a podcast, obviously.

In the bar at the Monte Carlo Bay Hotel, we gathered a crack group of sports media experts and asked them to dissect the big themes of the week.

Listen to Hugo Sharman, CEO of StreamAMG; Aarti Dabas of Formula E and Matthew Porter, CEO of PDC and chair of Matchroom Multisport here:

‘The market’s in a funny place’

This was Hugo Sharman’s point.

‘Which is why it’s the most interesting Sportel for years’.

And he’s right.

Simple stories and the limits of the fag packet

Much of the conversation is the direct to fan question, at every price point.

The OTT story is simple to understand.

Which is why it’s so beguiling.

Number of fans x Subscription fee = $$$

But the execution has proven complex.

Three years ago, Simon Jordan’s ran the numbers on Premflix, the oft discussed option of the Premier League going direct to fan.

"They are talking about bringing the product direct to consumer," added Jordan, "and that is exactly where they should go. They are talking about an audience of 200m around the world that are willing to pay £10 a month; I think that is a bit inflated and said 100m. That would bring in, under their model, £24bn a year - before they even talk about advertising and sponsorship opportunities. Compare that to the £2.7bn [they currently get]!”

But as Matchroom’s Matthew Porter puts it on the podcast:

‘You’ve got to be brave to turn your back on a multi billion dollar deal because some bloke somewhere has run the numbers’

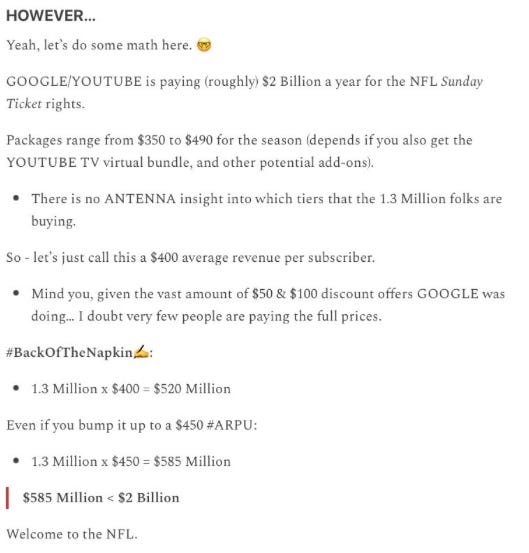

What’s Google’s game?

Google is paying $14billion for seven years of NFL Sunday Night Football.

The service launched last weekend.

DirecTV has had exclusive out of market rights since 1994, paying $1.5billion a year for the past eight years.

But…they lost fortunes on it.

So why has Google paid half a billion more a year?

Morgan Stanley think YouTube will lose $1.2bn A YEAR to 2029.

Good analysis by JohnWallStreet:

Reports have stated that just 10% of company subscribers bought the football specific service. It is challenging to make a direct business case for YouTube paying $2 billion a year to acquire the product given this context. And that is before one realizes YouTube is not requiring NFL fans to be YouTube TV subscribers to purchase their Sunday Ticket offering (as was the case with DirecTV). The streaming service can be bought on an a la carte basis.

However, Google may not be looking at it that way. The company may see investing in the tier-one produced content as a means of “driving more eyeballs and driving up CPMs to its traditional YouTube platform,” Matt Rosenberg (managing director & head of media finance, Monroe Capital) said. “Google can afford the large price tag it takes to do this.”

Sean McNulty gave good fag packet.

This prompted a fascinating exchange on WhatsUP, the Unofficial Partner private chat group, aka the best backchannel in the sports business.

@Adam Kelly/IMG: Any other opportunities to monetise 1m premium demo targets engaging v regularly on a digital service….?? Huge upside for Google

@Daniel Kirschner/Greenfly: Lots of reasons beyond straightforward subscription economics behind Google's purchase. YouTube is a powerful destination for finding sports moments from the past, but not the first place to go to find something live. As the streaming landscape becomes increasingly fractured—including with FAST services replacing RSNs in the US—content discovery will become a big challenge. Being a portal for all live sports would be lucrative for Google, both by charging partners and by driving more consumption's of Google's own offerings like Sunday Ticket. Beyond that, without opportune channel surfing or limited local offerings, right-holders will become increasingly focused on finding and developing new fans—customer acquisition—and what is more powerful than a platform like YouTube in steering people to new content based on existing interests. This will become incredibly valuable over time. And the ability to drive tune-in via key moments could be unparalleled. I can't tell you how many times I've turned on the final minutes of a game because the TV app on my iPhone prompted me about some exciting closing minutes.

@Peter Hutton: I’d add to that an ‘explainer’ that the NFL Sunday Ticket (which is largely what was acquired) is an add on to ‘You Tube Tv’, rather than ‘You Tube’. You Tube TV is not available in the UK but is the bundle of channels where the competition is largely local cable. It wins on price but loses on local sports (the RSNs are largely not available). Sunday Ticket gives an understandable point of differentiation to You Tube Tv from the traditional cable bundle and an argument for the sports fan to move across. As such, it’s very much the traditional sports as loss leader concept that we all know and love. Google will test and learn with it - but it’s not so revolutionary.

@Daniel Kirschner: Excellent point. In this way it looks like any other streaming service “overpaying”. Interesting and notable that you can get Sunday ticket standalone, at a price premium $449 vs. $349 if you have a YouTube TV subscription. And the unit economics, taken in isolation, don’t work at the higher price point. But the price differential gently pushes people toward changing providers for their streaming service (or cord cutting), and even if they don’t YouTube is gaining the subscriber relationship and insights on the standalone that it can convert down the road.

Talking about how much ESPN’s worth at the ESPN after party

Monday night at Sportel was an after party face off between ESPN and IMG.

The chat was about how much ESPN was worth?

This conversation was given some numbers to play with by last week’s release of rarely seen financial data.

There are many good financial analysts out there, but my GOAT is Bill Cohan.

I know ESPN is a fun and occasionally glamorous asset, but I just don’t think a rational financial buyer, or even a strategic buyer, would pay much more than $25 billion for it at the moment, and that’s slapping a healthy multiple of 9.6x my estimated 2023 EBITDA on the business. Besides the fact that the profits and margins are falling, there are also the two whopping problems that ESPN continues to face.

First, the cost of the live sports rights it depends upon are rising, as Nispel mentioned in his latest report, especially as the Apples and Amazons of the world enter the bidding market. ESPN has already committed some $45 billion to this endeavor through 2027, nothing to sneeze at. Second, ESPN also faces the death-defying problem of trying to convince cord-cutters to sign up for a revamped digital ESPN at some unknown price, at some unknown time. (Reports have suggested the package could cost anywhere from $20 to $35 a month and to start hitting the market next year.) All of which more or less adds up to the fact that $2.6 billion in 2023 EBITDA may end up being the high-water mark for ESPN. It still might be downhill from here.

Could Pitaro improve operating margins and convince millions to pay up for a digital ESPN while the cord-cutting slows? I suppose he could, yes. But, talented as he may be, that would require an extraordinary degree of finesse. I’m sticking with the $25 billion valuation for ESPN. And that’s generous.

Croker’s Partridge moment

“Murray, Murray, Murray…Murray?! Murray! Murray….Murray!”

Andrew Croker trying to get the attention of Murray Barnett, aka The Bundle’s Murray Barnett, while sitting at a roadside restaurant table in Monaco.

It turned out to be some random French bloke, so not the actual Murray Barnett.

SportelMan

Spoiler: There are lots of men at Sportel.

In fact, if listening to men talking is what you like doing, I can think of very few places you’ll like more than Monaco in October.

Men, stretching as far as the eye can see, talking at other men with the absolute confidence that comes from having the definitive OTT solution to meet your D2C needs.*

SportelMan can be identified by a uniform that pays homage to the ensemble modelled by Our Glorious Leader, God of All Football.

The Infantino Spring Summer Collection was out in force: Tight blue suit, white shirt, box fresh ice white trainers. Mmmm…sooo hot.

See also:

*Let’s play OTT WTF

Can you identify the OTT provider to their marketing strapline?

Much of the floorspace at Sportel is taken by OTT vendors of various shapes and sizes, all selling the D2C dream.

But which is which?

‘Stream, monetise and analyse every game’

‘Think big, stream bigger’

‘Leading sports content enabler’

‘Create your own OTT platform’

‘Feel the impact of reinvention’

‘From pitch to pixel’

‘We make sports grow’

‘Unlock the value of your media content’

‘From stadiums to screens’

‘Never stop inventing, yet keep it simple’

‘Own your audience’

‘Turnkey live production and distribution’

Hear also: What’s the difference between a good OTT provider and a bad one?

New Series, launching soon: ‘I’m no sports IP lawyer but…’

In which the logos of upstart new sports properties are compared to those of other, more famous sports properties.

Episode 1: Major League Paintball vs Major League Baseball

Inside the life of a podcaster

It’s not all shit and giggles. Sometimes it’s avoiding work by hiding out in a posh hotel.

The Monte Carlo Bay Hotel is very lovely btw.

See you there next year?

Press the Like button below or we kill a puppy.