The new language of the sports biz: Dry powder, distressed assets and paths to liquidity

Words and phrases to use when talking Bankspeak™️

It’s heating up out there isn’t it, you can feel it. There’s a ton of money sitting around, just waiting to be spent in sport and there’s a corresponding shift in the language. Let’s call it Bankspeak™️. Defined as words and phrases that are becoming part of the sports business conversation: Ocean Front Properties, dry powder and fundamental illiquidity.

I’m indebted to Kyle Charters of Inner Circle Sports for helping me decipher some of it. (Hear our conversation on the last Money Talks pod, which landed last week, and thanks too to Dan Connolly for connecting us).

First some context. John Wall Street had a good primer on the money flushing around the VC market. And he put some numbers to it.

The general sense that cheap money is looking for a home is backed up by anecdotes. This one from Leeds Utd owner Andrea Radrizzani is one of several (via @shaymantim’s Twitter feed)

As mentioned on a previous newsletter, the Money Talks series is my safe space to ask dumbass questions to people who know about money and can help me decipher Bankspeak. And already, three episodes in, patterns are emerging, and my questions are getting a little more specific.

The argument in favour of billionaires

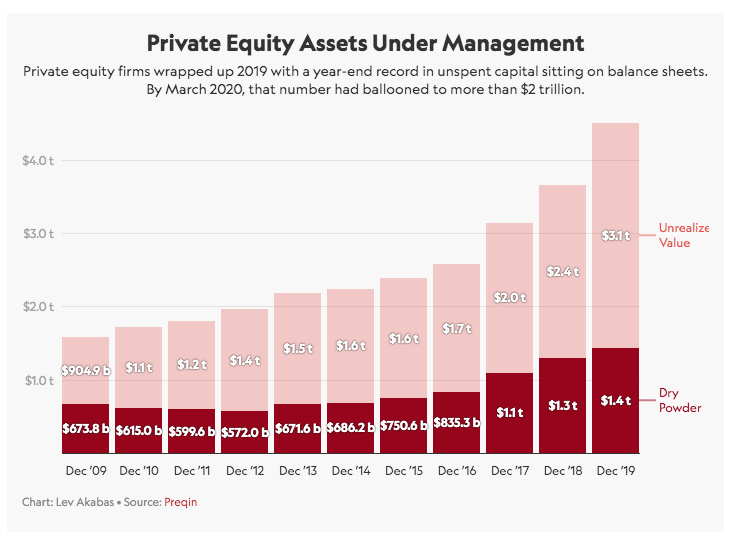

How does $2trillion get spent? And, if you’re in sport, what type of money do you want to buy you? The sourcing question feels so central. Sports teams are inherently illiquid assets to own, meaning they’re hard to get rid of once you’ve bought them. If you buy Apple or Walmart stock, you can sell it again an hour later if you lose your mojo. Buy Spurs from Joe Lewis and you’re stuck there for a while, good and bad.

So what? Here’s Kyle Charters on why the illiquidity of sports teams shapes the conversation.

When you’re a P/E firm you have limited partner capital behind you, often teaching unions or pension funds that are solely driven by financial returns. So, in the jargon, they must have a path to liquidity. They will give you a dollar and expect to get two dollars back, and the sooner they can get that two dollars back the better. A family office has a more generational, long term view on their capital, so historically they are better aligned with sports and the dynamics of sports ownership. The leagues also like billionaires. Stability is incredibly important for the leagues, the last thing they can have is a revolving door of owners.

So billionaires are a safer bet and the leagues like them because they hang around longer, making them look good. Or put another way, they have enough money not to have to worry about high returns. But they don’t want to have to explain to other billionaires when they buy something and then getting relegated (see: Shad Khan/Fulham)

Flip the ownership conversation to a US Major Leagues v European soccer clubs standoff. In the US there’s an oversupply of billionaires, or in Bankspeak ‘Sophisticated family offices’, who are seeking ‘Ocean Front Properties’ (love this analogy):

The supply demand dynamic is completely flipped. In the US there are only a small handful of true change of control opportunities every year, if that. So there’s a huge demand and very little supply, also known as the Ocean Front Property problem. If you want a place on the sea, you’re going to have to pay big.

In Europe, it’s a different model, with risks around relegation, which has created an inverted supply and demand dynamic. With the exception of the top 20 or so clubs in Europe there is some opportunity to transact at the right price.

So most European football clubs are permanently for sale. But there’s only so many billionaires and well capitalised investors ready and informed enough and willing to taken on the risk of relegation. A further thought relates to whether the American Major Leagues are in a better position to be able to scrutinise every owner and potential owner and run them through a detailed vetting process. In Europe, there’s less leverage - fewer potential buyers. So they can’t be as picky?

An old friend who never went away: The European Breakaway League™️

The money conversation leads to an obvious endpoint. The money in John Wall Street’s graph above is waiting for European football to become a closed shop. At that point, a gold rush ensues as American billionaires and private equity shops go in search of European football clubs.

‘If you buy a MLB team and the team has a couple of bad years, that franchise is not getting sent down to Minor League Baseball. In Europe you take on that risk from day one. And relegation is an economically transformative moment in the negative (Editor’s note: this is also known as Shit Creek).

So, is CVC in rugby just about security. They can see a closed future for the Rugby Premiership, the Six Nations etc, which for the time being is not happening quickly enough for them in football.

The problem with the Silicon Valley Startup Story (SVSS)

Pet theory. Most sports and business journalists, including this one, don’t really understand how finance works, so they fall back to stereotypes and story shapes that hint at insider knowledge. ‘Private equity eyes sport’ headlines quickly frame stories that follow the Silicon Valley Startup shape: in and out in five years, turning one dollar in to 5x or 10x. (Other bits of this mythology include feature interviews with the Charismatic Founder, in the Steve Jobs, Jeff Bezos mould).

But sports teams don’t fit the SVSS shape.

Sports team values have escalated over the past decade…but it’s not a venture-like return. You should never go in looking for 5x or 10x return no the money, it’s just not that sort of investment. The beauty of buying an NBA team is you have very little downside. As long as you believe in the long term value of the sport and its content, and by extension its relationship as a valuable media product, your money is safe. It should be a steady climb up and to the right.

Butts and seats, adjacencies and the importance of 2014

Feature idea: 2014 is the most significant year in sports tech since the first dotcom boom.

Like all story pitches, this has its flaws, but let’s focus on the gist.

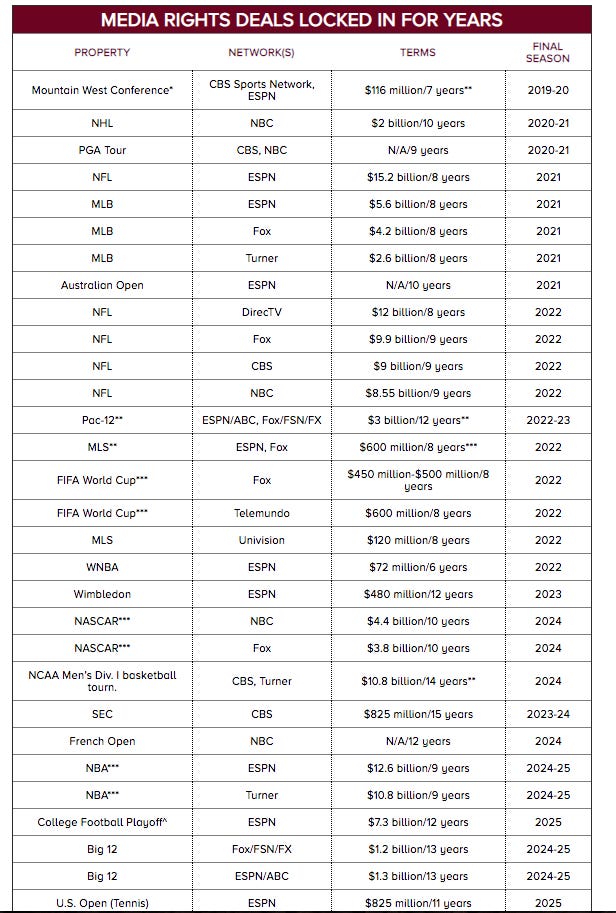

Digital transformation saw a marked uptick among US leagues and franchises after 2014, a year when many long term media rights deals were sealed, giving them security and time to plan.

Is the slowness of the transition due to long media contracts? They just didn’t need to change, mother of invention. It’s just not as pressing.

The 2013 there was a big wave of media rights signed, and a lot of the leagues shifted focus on other areas, which has led to a vibrant tech sector adjacent to sport.

Kyle Charters:

Closed leagues and the long term media rights income has created certainty, and new markets for investment. The teams have grown their own budget and have revenue backed by long term contracts and look out several years and have security as to what the profit and loss statement will look like. The impact of that has been to enable teams and leagues and governing bodies and broadcasters and gambling firms to invest in technology and other services.

What used to be quite a sleepy ‘butts and seats, selling merch and beer’ type of business in to a long term media driven ecosystem. Some teams can outlook 60% of their income in long term contracted media rights.

So a cottage industry of digital and tech enabled service providers has appeared because the teams had the money - and foresight - to know they had to change and therefore fund them.

Proof point: A graph of major US media deals signed in 2014

The Financial Upside of Dozy Luddites

To the earlier point on my own ignorance, this was exposed by a question on the podcast when I framed the failure of various sports to jump on the digital transformation train as a problem for investors. This is 100% wrong. That’s not a problem, that’s the opportunity.

Investors will look for sleepy, non-technologised industries. The sports industry is historically low and slow on the tech adoption spectrum. It’s an industry that’s been change and risk averse and over the past few years has been forced to change, accelerated by Covid. Investors see optimisation with the new world we live in. There’s still a lot of room to be enabled by technology, it’s still pretty heavy on manual workflows, communications supported by paper and cell and email. So a lot of the tech replacing that infrastructure has only been coming in to sport over the past five to eight years. Fifteen years ago, the way the Boston Red Socks sold tickets was very different than it is today. Chelsea do internal comms is different then and now.

So, billionaires will buy teams and VCs will buy adjacencies, aka data agencies and esport stuff?

Can you see the pattern?

Td;lr Nothing’s new under the sun.

We have some pattern recognition. We did this in healthcare, or waste management or food and beverage, that happened five to eight years ago that is only now happening in sports.

Private equity and sport, cont’d.

Finally in this money thread, it’s been a good week for billionaires. Two of Britain’s biggest columnists came out in their favour.

The first was Martin Samuel in The Daily Mail in the context of Man City’s FFP hooha.

Check out the opening line…

Owner investment does not kill competition: it creates more. The penny is beginning to drop over what is being attempted here. Wolves, having signed the original letter to CAS, are understood not to have been part of Monday's group call. Everton and Sheffield United were always outside the conversation. Why would they lobby to wrap ambitious clubs in red tape, stunting their growth and leaving them at the mercy of predators?

The big lie of FFP is that clubs should grow organically. Yet how is that possible if a middling organisation cannot invest further to compete, while its best players are poached? Leicester won the League and lost N'Golo Kante to Chelsea that summer. Ben Chilwell is likely to travel the same route this year.

Southampton could have been an outstanding team across the last decade, maybe another Leicester, but were denuded by Liverpool and others. FFP kills challengers.

There is no other industry that does not allow competition from companies injecting capital to improve performance and output.

If Saudi Arabian investment now makes Newcastle a force, how is that bad for the game? Don't Newcastle fans deserve that? Isn't the city worthy?

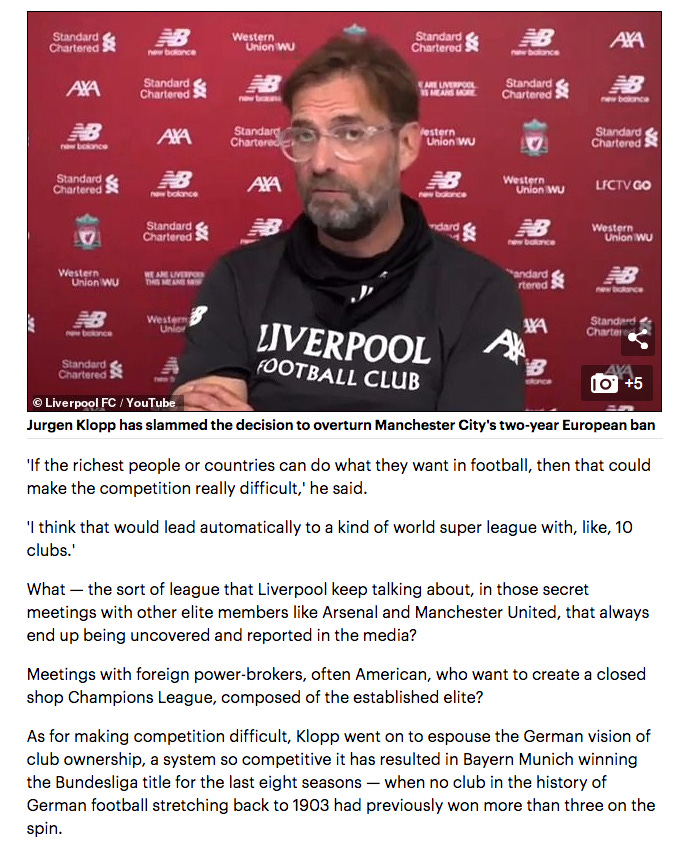

Featuring..Jurgen Klopp on the European Breakaway League™️

Finally, Daniel Finkelstein (@dannythefink) in The Times. A nice piece on Jack Charlton’s passing, which managed to frame Big Jack’s career as the story of capitalism versus socialism. A nice volte face here, again jumping off FFP:

What a contrast his straightforward style provides to the tawdry financial shenanigans of modern football. And what better example could there be than the decision, announced on Monday, that Sheikh-owned Manchester City will not face serious punishment for what seemed to be obvious breaches of football’s financial rules.

Journey from shambolic amateur sport

Yet the more one studies Jack Charlton’s life, the more one questions this verdict. In fact, his true greatness lay in the steps he took from the shambolic amateur nature of the sport he joined to the extraordinary professional spectacle it is today.

This story of progress isn’t unique to football, by the way. It’s the story of many other sports but also of our country more generally. For all the defects of big-money sport, and indeed big-money capitalism, the journey of the last century has been towards the light.

Joining Leeds at the age of 15 did not involve the club in careful nurturing of precocious talent. Instead it involved a little training and many more hours of cleaning lavatories, oiling turnstiles, restudying boots and inflating balls. Then, shortly after Charlton finally appeared for the first team (an event that arrived by surprise, without any words from the manager and with no advice about what he was supposed to do) he was sent away for two years of national service.

As Charlton said about that experience (which, to be fair, he remembered fondly): “I learned all my bad habits in the army, and smoking was one of them.” He carried on smoking for the rest of his professional career.

Never mind allowing players to smoke, Leeds in the second half of the 1950s didn’t talk to their players much at all. They didn’t employ a coach. They didn’t practise corners or free kicks, they didn’t really have team talks or a run-down of the opposition line-up.

Meanwhile, players with young families needed to do other things to make ends meet. As an England international on his way to winning the World Cup in 1966, Jack was selling cloth to his fellow England stars from the boot of his car. Later he set up a souvenir stall outside the Leeds ground and his wife sold scarfs to fans.

The allocation of tasks in football was extraordinary. In his first managerial job, as the boss of Middlesbrough, one of the world’s greatest football strategists spent his time buying paint for the stadium gates and personally delivering fixture sheets to local offices and factories to be placed in their canteens.

All this may have romantic appeal but contrast it with the modern game with the way that talent is nurtured, fitness is honed, pitches are tended, players are scouted, tactics are developed, data is used; with the way that players are guided and supported, helped to plan their careers, allowed to concentrate on the game. Even with the way souvenirs are sold.

The sporting advantages of the big money that has come into the game are obvious. The cash has brought professionalism and that in turn has brought better sport. Football is faster, more skilful, better officiated, more (not less) sporting and played in better stadiums on better pitches. A young Jack Charlton would now be seen as an asset and businesses look after their assets.

Big money equals big advances

You can see the same trend in other sports. Tennis, for example. Elite players are now fitter, the game has become more powerful, rackets have evolved, and the median age of the top 50 tennis players keeps rising as the investment in physical strength pays off. And as the financial impact of bad calls increases, technology has developed to improve umpiring.

So, yes, the way money is raised and spent in some Premier League football clubs is a matter of concern. And yes, if you set rules you have to police them properly and the football authorities seem pretty hopeless at it. But the big money that has gone into the game has been far more positive than negative.

And, in any case, if you wanted to stop it, every sport would have to participate, which is hardly likely. Take the salary caps in rugby that led to Saracens having a huge points deduction for violations. If a young person capable of an elite professional career can choose any sport, why would they choose one with a capped salary? The evidence is that they would gamble on their talent.

Or take the Olympics. One of the great moments in the modern Games was the 1992 victory by the US basketball team that included the mega-salaried Michael Jordan and Magic Johnson. It was also the moment when it became plain to all that you could either have highly paid professionals who were the very best or amateurs who weren’t.

Till next time. Before that, check out Dugout’s Elliot Richardson on All Models Are Wrong talking digital and football, and Simon Oliveira on Beckham and fame. I’ll fill in the gaps in a future newsletter.

Spread the word.

R