What's Klopp worth; LFC were too big to fail; RBS guide to risk capital; The real LIV CEO; The ultimate bundle piece; Fixing rugby; Rich get richer shock; Social media in China, the cheatsheet

Overthinking the sports business, for money

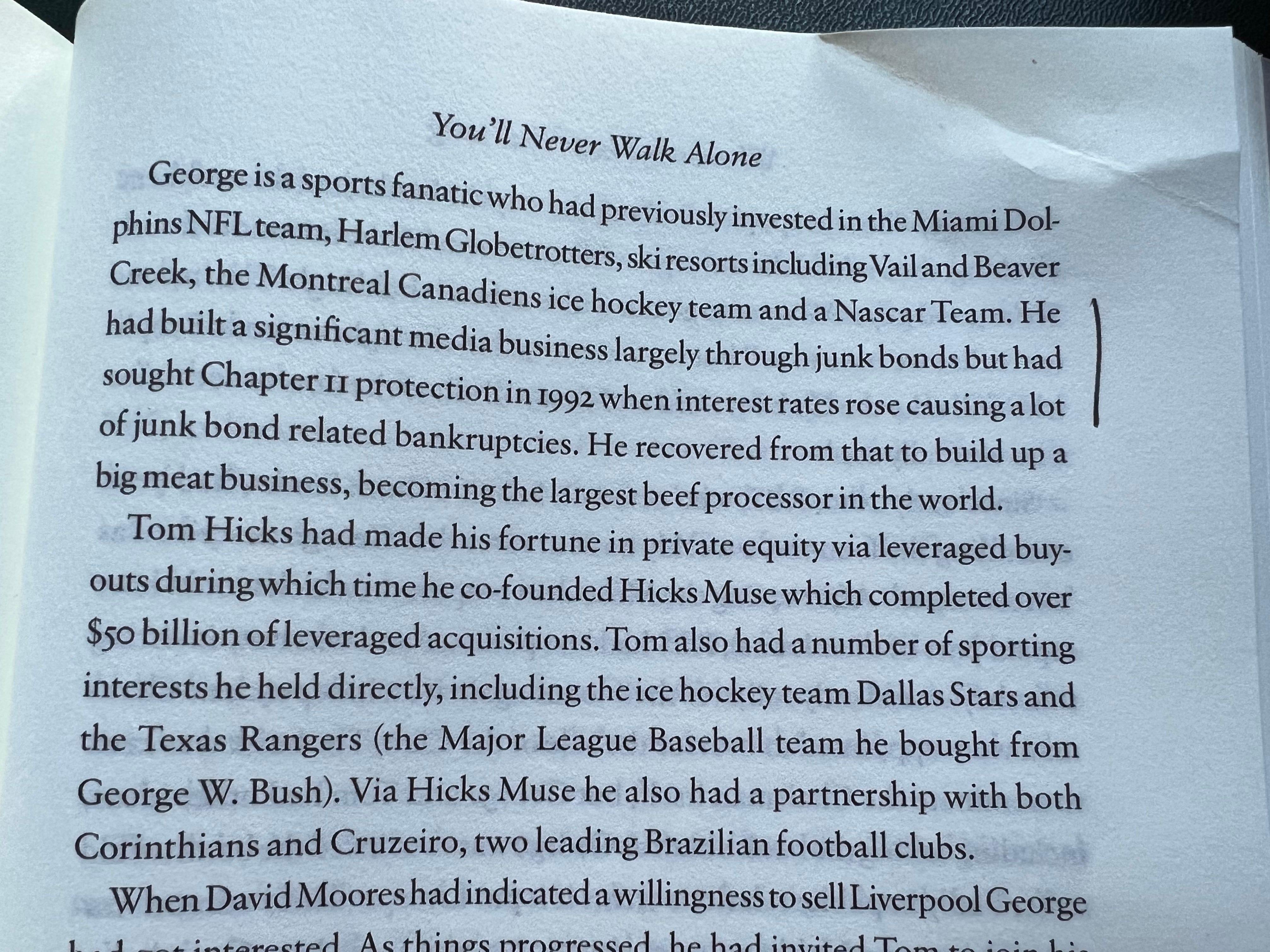

What’s a Premier League club worth?

If anyone knows the answer to that question it’s Sir Martin Broughton.

He sold Liverpool and nearly bought Chelsea.

We’ve just spoken to him for an upcoming podcast.

The timing’s good, given the regulator conversation.

Some conversation starters:

How much of the value of Liverpool is attributable to Jurgen Klopp?

Liverpool has been sold twice in the last twenty years. So we have two real valuation moments.

2007 - £219million (Moores family to Tom Hicks and George Gillett)

2010 - £300million (Hicks/Gillette to Fenway Sports Group)

There’s speculation that FSG is seeking a buyer (with the caveat that this may be a kite flying exercise prompted by the Chelsea sale).

Regardless, its fun to speculate on the current price point of Liverpool FC.

2023 - £2 to 4billion??

So a 10x increase in 15 years.

Going back to the initial question, how much of that increase is due to on field success and the associated brand value that comes with it?

Or is onfield performance just noise; a marginal contributor to value, the bulk of which is about media rights outlooks and theories around monetising fan bases at home and abroad?

In other words, what would the price of Liverpool be if Roy Hodgson/Brendan Rogers/whoever was still in charge, and the club had spent the last few years in mid to high table obscurity - no Champions League win, no Premier League title.

What the fuck were RBS doing?

Hicks and Gillette funded their purchase of Liverpool by a 100% loan from RBS and to a lesser degree, Wells Fargo.

This is how Broughton puts it:

‘Given their background it was no surprise to learn that neither of them had invested any of their own money at the time of purchase. They borrowed the entire £219million from Royal Bank of Scotland but also from Welsh Fargo Bank. Crucially, they had promised the Liverpool fans that the debt was not a debt of the football club but their own debt held via a holding company, called Kop Holdings.’

That phrase ‘Given their background’ is worth exploring further.

This from Broughton’s book. The word leverage comes up a lot:

Two years later the financial crisis did its thing and the dynamic duo were left naked as the tide went out, which is Buffett speak for being massively over leveraged, buying stuff with OPM.

This prompted RBS to demand their money back, which of course they didn’t have. And hilarity ensued.

Liverpool were too big to fail

This is where the football business is different.

To get their money back, RBS would need to put Liverpool in to administration.

Imagine the headlines.

Bailed out bank bankrupts famous football club. Fans take to every RBS branch in the country.

So they fudged, got Broughton in as chair, and gave him six months to find a buyer, which he did.

Gold v Digital Gold

“It wasn't digital gold, it wasn't a hedge, it wasn't a store of value – it was a tech, risk-on mega bubble bet, helped by easy money. And so when the easy money goes away, that bet falls.”

Lionel Laurent, Bloomberg Opinion columnist

Ben Thompson just wrote the definitive article on bundling

See also: From The Four Myths of Bundling

The way they’re described here, SuperFans share many characteristics with drug addicts.

See also: What is a festival?

A build on previous conversation on entertainment bundles.

a man told me he had stopped going to Latitude the year they put bars in the performance tents. ‘It wasn’t just that you had to pay £8 for a pint. They introduced people who would stay in the queue for you, for another £4, so you could keep watching. I felt like I was being bled dry.’

Fixing rugby

If you started again, back to 1995 when the game went pro, what would you do differently?

Then explain why you don’t end up with closed leagues for the club game.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

Spreadsheet of the Week: His Excellency Action Tracker

Hidden in the PGA Tour v LIV court filing.

Note the reality of power behind the scenes at LIV.

The LIV Effect

The latest iteration of the PGA Tour’s response to LIV came out this week.

Spoiler, the rich will get richer.

One of the richest - Rory McIlroy - explains why this is a good idea.

Note the reference to what Mastercard wants (him), and the desire for golf to be ‘aspirational’ (him again).

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

The big winners appear to be the four Majors.

The PGA of America gave clearance for LIV players to compete at the 2023 PGA Championship — meaning that LIV golfers are now eligible to compete at all four majors this year.

For the PGA of America, Augusta National, the USGA, and the R&A, the reasoning is obvious: The four majors are currently the only tournaments featuring the top players from both the PGA Tour and LIV Golf, creating a Super Bowl or World Series type of atmosphere at each one.

I’ll point you in the direction of a previous note, making the same point about tennis: Slams Assemble.

Many of the problems now being tackled by Jay Monahan were set out in our podcast with Andy Gardiner of the Premier Golf League.

The difficult question for Monahan is why did it take a breakaway to make him bring in changes?

A cheat’s guide to social media strategy in China

Courtesy of Mailman’s new report.